If you’ve found yourself wondering what insurance you should get or what insurance is right for you, then you’re not alone.

Whether you’re a rider, a delivery rider, or a commuter, choosing the right motorcycle coverage can feel overwhelming. Third party? Fully comp? Add-ons? Cheapest option?

In this guide, we’re going to run you through what it all means and what you should consider when choosing the right insurance for you.

So, let’s get into it!

The Different Types of Motorcycle Insurance & What They Cover

First of all, it's important to note the three main types of motorcycle insurance in the UK.

Third Party (TPO)

This is the legal minimum. You will not legally be able to ride your motorcycle without this on UK roads. It pays for damage or injury you cause to others, but not for damage to your own bike.

If you’re at fault in an accident, your repairs come out of your pocket.

Third-party, Fire & Theft (TPFT)

TPFT includes everything in Third Party cover but also protects your bike if it’s stolen, damaged during an attempted theft or damaged by fire. It’s a popular middle-ground insurance option, especially for riders who park on the street or want extra peace of mind without going fully comprehensive.

Comprehensive

Also known as fully comprehensive motorcycle cover. Comprehensive cover includes everything in Third-party, Fire & Theft, plus protection for damage to your own bike — even if an accident is your fault.

It’s the highest level of motorcycle coverage and often offers the most peace of mind (and surprisingly, it isn’t always the most expensive option).

How do insurers calculate the sum of your bike insurance policy?

When you get a motorcycle insurance quote, insurers look at a variety of factors to figure out how likely you are to make a claim. These factors include:

- Rider Information (Age, claims history, licence type etc)

- Bike Information (Make & model, engine size, value, modifications etc)

- Policy details (Level of cover, voluntary Excess, Payment method)

- Number of riders

- Previous driving experience

Typically, the higher the risk, the higher the premium.

Which Motorcycle Insurance is Best for You | Factors to Consider

Choosing the right motorcycle insurance isn’t about picking the cheapest quote and calling it a day. It’s about finding cover that fits how you ride, what you ride, and why you ride.

Here are the key factors to think through before you lock in a policy...

1. What type of licence are you riding on?

So, what licence are you riding on? A provisional or learner licence? Insurers often see newer riders as higher risk, which can mean higher premiums or specific policy restrictions.

If you hold a full motorcycle licence, you’ll usually have access to a wider range of policies and more competitive pricing.

2. Usage of your Bike

How you use your motorcycle matters just as much as what you’re riding.

- Commuting: If you ride to and from work regularly, your policy needs to include commuting use.

- Social, Domestic & Pleasure (SDP): This typically covers leisure rides, weekend trips, and non-work-related journeys.

- Business Use: If you travel between job sites or use your bike for work purposes beyond commuting, you’ll need business cover.

- Delivery Riding: If you’re working as a courier or food delivery rider, standard insurance isn’t enough. You’ll need specific hire and reward or delivery insurance. Riding without it can leave you completely uninsured during work hours.

3. Estimated Mileage

You’ll be asked for your estimated annual mileage. A rider covering more miles a year is generally going to be at more risk.

Be realistic when estimating. Underestimating mileage to save money can backfire if your usage is clearly higher in the event of a claim. The insurer could increase the price or even reject the claim, so make sure if your riding habits do change mid-policy, you update your insurer.

4. Make & Model of your Bike

Your motorcycle’s make and model significantly affect your premium.

High-performance sports bikes, for example, are generally more expensive to insure than smaller commuter bikes due to higher repair costs and theft risk.

Insurers look at:

- Engine (cc)

- Performance and top speed

- Repair and parts costs

- Theft statistics

- Safety and security features

The exact model matters too; even two bikes from the same manufacturer can fall into different insurance groups depending on specifications.

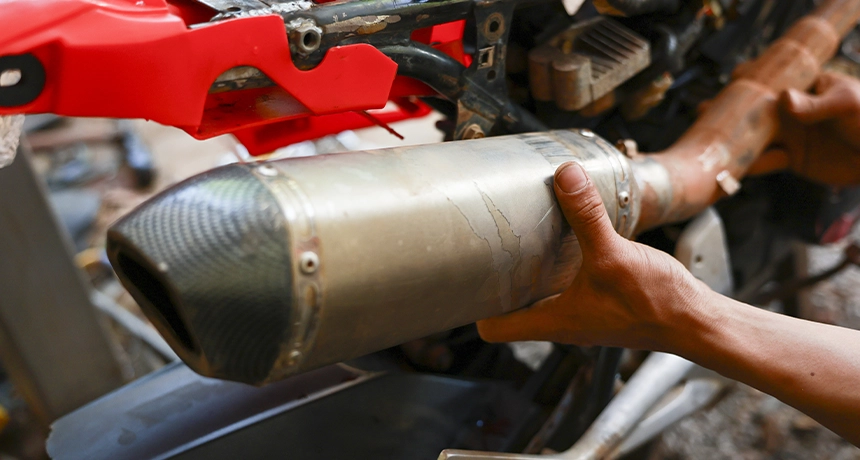

5. Does your Bike have any modifications?

Modifications can affect both your premium and your cover, so always declare them. Some insurers may even decline a quote subject to what the modifications are.

Common modifications include:

- Aftermarket exhaust systems

- Performance upgrades

- Cosmetic changes

- Custom paintwork

- Suspension changes

Some modifications increase performance, which may raise your premium. However, things like approved security upgrades could lower it. But make sure to always double-check with your insurers first before making any changes, as your policy may be voided.

If you do not declare any of the modifications of your motorcycle and make a claim, your insurer could reduce the payout or reject it altogether. It’s always safer to be upfront.

5. Where do you store your Bike?

Where your motorcycle is kept overnight can significantly impact your insurance premium.

Bikes stored in a locked garage are generally considered lower risk than those parked on the street. Secure off-road parking, private driveways, and gated properties can also reduce the likelihood of theft or vandalism in the eyes of insurers.

6. How much excess are you willing to pay, in the event of a claim?

The excess is the amount you agree to pay toward a claim before your insurer covers the rest.

There are usually two types of excesses, these are:

- Compulsory excess (set by the insurer)

- Voluntary excess (chosen by you)

Choosing a higher voluntary excess can reduce premiums. However, it also means you’ll pay more out of pocket if you need to claim. The key is balance; select an amount you could realistically afford if the worst happens.

7. Do you Hold Any NCB? (No Claims Bonuses)

A No Claims Bonus (NCB) rewards you for claim-free riding, having earnt this in the UK. Even one year of NCB can reduce your premium, and multiple years can lead to great savings.

If you’ve built up NCB on a previous motorcycle policy, make sure you declare it. Some insurers may also offer NCB protection for an additional fee, allowing you to make a limited number of claims without losing your discount.

8. Do you intend to carry a pillion?

If you plan to carry a passenger, even occasionally, your policy must include pillion cover. Not all policies automatically include this, particularly for learner riders. Carrying a passenger without the appropriate cover could invalidate your insurance.

Even if you rarely take a pillion, it’s worth confirming the policy wording to ensure you’re properly protected.

9. What Security Measures do you have for your bike?

Motorcycle theft is a major factor in insurance pricing and policy conditions, so security matters. If the insurer's security requirements are not met and your bike is stolen, the insurer has the right to invalidate any claim.

Common security measures include:

- Approved disc locks

- Heavy-duty chains and ground anchors

- Alarm systems

- Immobilisers

- Tracker devices

Using insurer-approved security devices can sometimes reduce your premium. For example, an insurance-approved motorcycle lock or tracker.

10. What to do if your Bike is declared as SORN

If you’re not using your motorcycle and it’s off the road, you may declare it as SORN (Statutory Off Road Notification).

Once a bike is SORN:

- It must not be ridden or parked on public roads

- You are no longer legally required to have road tax

- Standard road insurance is not legally required

However, cancelling insurance entirely may leave your bike unprotected against theft, fire, or accidental damage while stored. Many riders choose to switch to laid-up insurance, or even fire and theft cover instead.

Other Insurance Add-ons to Consider

A few add-ons can make a big difference when the unexpected happens…these extras aren’t always necessary, but for many riders they offer valuable peace of mind.

Here are some of the most common optional extras to consider:

Excess Protection Insurance

If you need to make a claim on your policy, you’ll usually have to pay an excess amount towards the cost. Excess protection insurance can reimburse you for this payment after a successful claim, helping to reduce the out-of-pocket expense.

Breakdown Cover

Breakdown cover assists you if your bike stops working while you’re on the road.

Depending on the policy, this can include roadside repairs, recovery to a nearby garage, or transport for you and your motorcycle if it can’t be fixed at the scene.

Helmets & Leather Insurance

Riding gear can be expensive to replace. Helmets & Leather Insurance covers exactly what the name suggests. Providing cover for the cost of items such as helmets, leathers, gloves and boots if they’re damaged, stolen, or lost following an accident or insured event.

Personal Accident Insurance

Personal accident cover provides financial support if you’re seriously injured in a motorcycle accident. Policies may offer a payout in the event of permanent injury, disability, or death, helping to support you or your family during difficult circumstances.

Most Common Motorcycle Insurance Myths | Busted

Motorcycle insurance can be confusing, but it’s important to know that not everything you hear/may think is always accurate.

Fully Comprehensive Insurance is Always the Best

Fully comprehensive cover does offer the highest level of protection, but that doesn’t mean to say it's the best option for everyone.

The right policy depends on factors like the value of your bike, how often you ride, and your budget. Riders may choose third-party options if they feel the extra cover isn’t necessary.

Third-party insurance is the Cheapest

Many people assume third-party insurance will always be the lowest price because it provides the least cover.

However, insurers set premiums based on risk, and sometimes fully comprehensive policies can actually come out cheaper depending on the rider’s profile and the bike being insured.

NCB on Car Policies Can Always Transfer over to your Bike Policy

No claims bonus (NCB) earned on a car policy doesn’t automatically transfer to a motorcycle policy.

Some insurers may recognise it in certain situations, but many treat car and motorcycle insurance separately.

You don’t have to inform your Insurers of Modifications

Any modifications to your motorcycle should be declared to your insurer.

Changes such as exhaust upgrades, engine modifications, cosmetic alterations, or performance parts can affect the risk profile of the bike. Failing to declare them could potentially invalidate your policy.

If you are convicted of a riding or driving offence during your policy, you do not have to tell your insurers

If you receive a motoring conviction while your policy is active, you’ll usually need to inform your insurer.

Many policies require this as part of the terms and conditions, and not letting them know could affect future claims or renewals.

Naming another rider on your policy will bring down the cost

Adding another rider doesn’t always reduce the cost of insurance.

In some situations, it may help if the additional rider is experienced, but in other cases, it could increase the premium depending on their age, experience, and driving history.

Insurance premiums automatically go down after each year

Premiums don’t always decrease over time.

Whilst building a no-claims bonus can help lower costs, other factors, such as changes in risk, inflation, claims trends, or personal circumstances, can still affect the price at renewal.

If I lower my annual mileage, it will make my insurance cheaper

Lower mileage can sometimes reduce premiums because the bike is on the road less often.

However, it isn’t guaranteed to make your insurance cheaper, as insurers consider many different factors when calculating the cost of a policy

The Last Stop!

So, there is our guide to helping you understand what you should look for and consider when choosing the right insurance for your motorcycle! And now that you’ve learnt a thing or two, and know what you’re looking for, make sure to get a motorbike insurance quote directly with Lexham!